Avoid This Dangerous Way of Picking Investments

William Barreca - Jun 04, 2024

When choosing an investment, the temptation to chase recent winners is pervasive.

Whether it's individual investors or professionals in the financial industry, the allure of stellar performance can cloud judgment. However, as we'll explore, past success does not always indicate future gains.

As long as investing has existed so have star fund managers.

Consider Cathie Wood, the renowned figure behind ARK Investments.

During the height of the pandemic, her speculative technology stocks experienced a meteoric rise, making her a star in the investment world.

However, fast forward a few years, and the tide has turned.

Unfortunately, many investors fell victim to the hype and invested right around the February 2021 peak, shortly before her meteoric performance dropped back to earth.

The website Morningstar found that her ARK Innovation ETF has been the 3rd largest wealth destroying fund over the last decade, losing investors $14.3 billion.i

This outcome was entirely predictable and underscores a crucial point: past performance is not always indicative of future success.

History is filled with star fund managers who couldn't sustain their performance for extended periods.

Why does this happen?

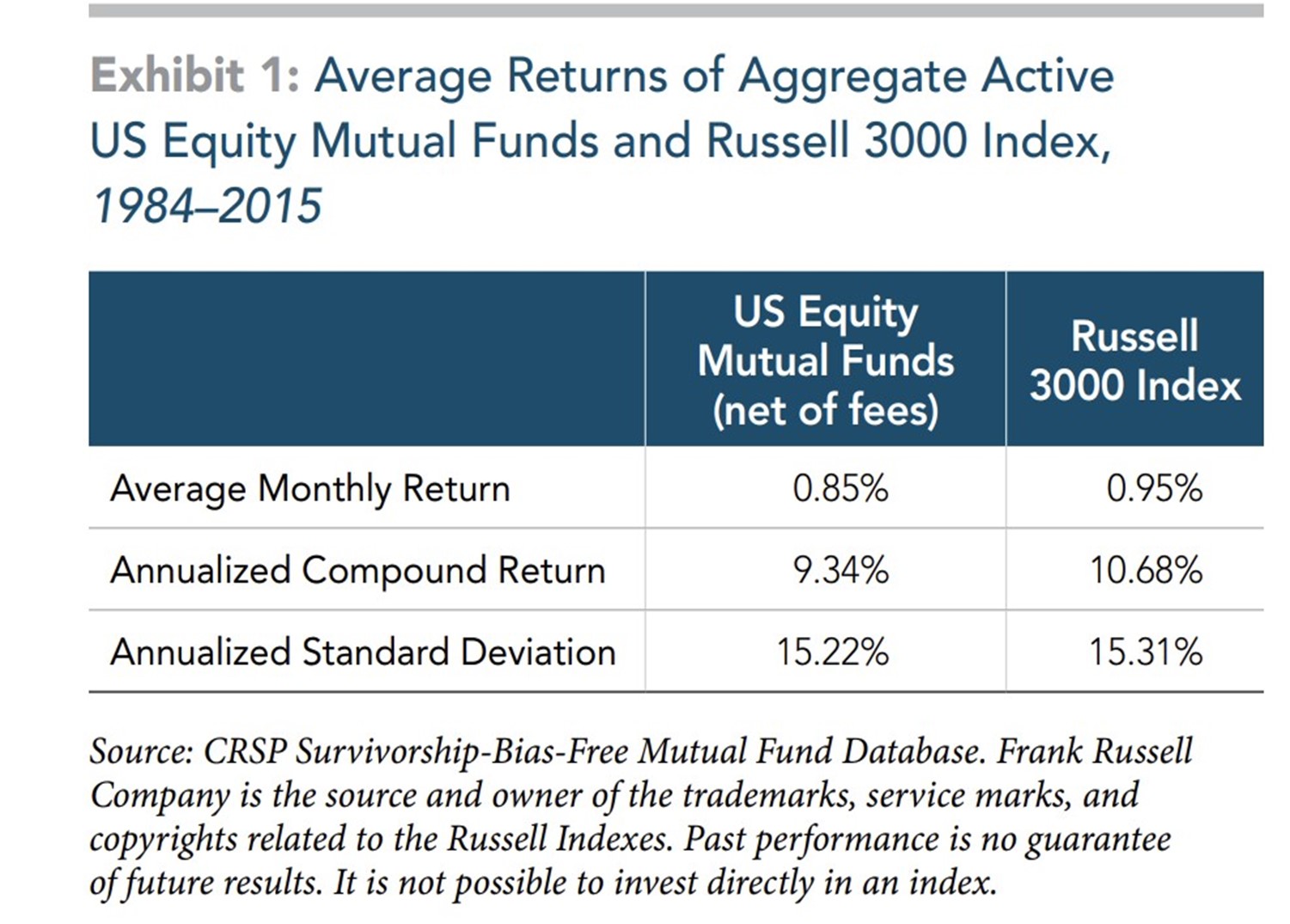

Historically, active stock-picking strategies struggle to outperform their benchmarks.

A common thing I hear is that people should pick the "best" managers.

This sounds good, in theory. The problem is separating luck from skill when evaluating a manager.

Anyone picking stocks can get lucky in a short time. The key is sustaining performance over long periods.

Academic research, notably the landmark 2010 paper by Eugene Fama and Kenneth French, studied this in their landmark 2010 paper "Luck versus Skill in the Cross-Section of Mutual Fund Returns."

Their findings suggest that while some managers may appear skilled based on short-term performance, it's often difficult to discern luck from true skill. Moreover, the majority of active funds fail to produce benchmark-adjusted returns that cover their costs, indicating that sustained outperformance is rare.ii

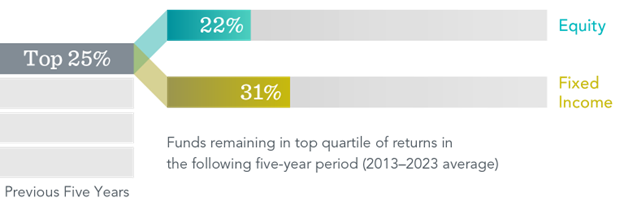

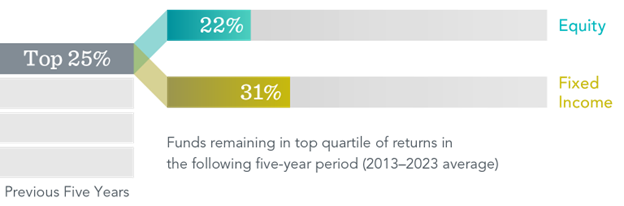

Further studies support these conclusions, showing that of the funds ranked in the top 25% based on five-year returns, only about one in five equity funds remained in the top 25% during the next five years.

iii

iiiThe implications? Those who select investments based on past returns are likely to be disappointed.

This should demonstrate that a fund's past performance does not indicate its ability to continue that performance.

All things being equal, a strong-performing fund should be expected to underperform in the future relative to its benchmark.

*The views and opinions expressed in this article may not necessarily reflect those of IPC Securities Corporation.

ihttps://www.morningstar.com/funds/15-funds-that-have-destroyed-most-wealth-over-past-decade

iihttps://mba.tuck.dartmouth.edu/bespeneckbo/default/AFA611-Eckbo%20web%20site/AFA611-S8C-FamaFrench-LuckvSkill-JF10.pdf

iiihttps://my.dimensional.com/3-common-investing-mistakes?_cldee=x0Wa0787g88F0URjL2qajTYMAZqeM87lC0fWAo2kAeoGUbhsL3gG2cd9eammBCXm6661yvLXGY9bXO37Tafh9Q&esid=ebccbff9-1907-ef11-9f8a-000d3a3431b4&recipientid=contact-27b38883d64bed11bba1000d3a3431b4-